The Tax Cuts and Jobs Act of 2017 significantly expanded the federal definition of qualified expenses for 529 plans (withdrawals free of federal taxes and penalties) to include not only higher education expenses, but also up to $10,000 a year toward the cost of private K-12 schools. This major change in the federal tax code has significant implications for states, and state policymakers have some difficult decisions ahead.

Here’s why: Over the years, many states have added a variety of state-specific incentives to the 529 plans they offer, including matching funds (12 states) and tax deductions or credits (35 states). These incentives assume parents are saving for college over many years. What will it mean for such funds to be used for K-12 expenses? How might it impact the return on investment of 529 plans for parents and states, or the dollars available for public school funding in the state?

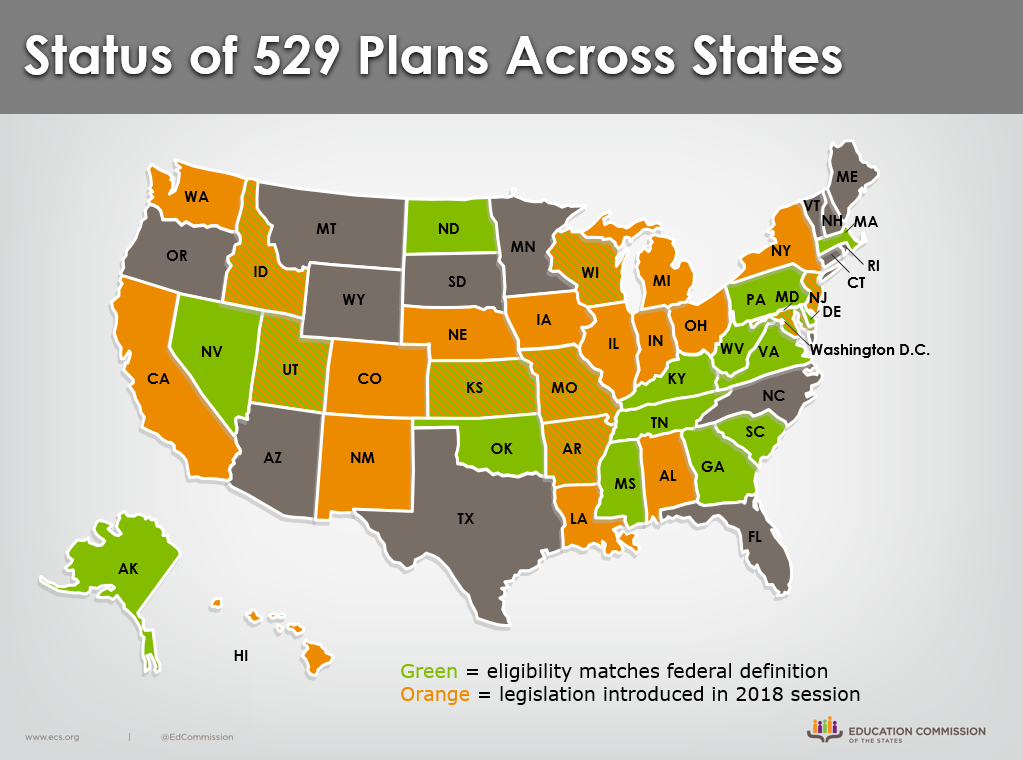

States are currently grappling with these questions. The 2018 legislative session has seen a flurry of activity on the issue, with nearly 70 bills introduced across 23 states related to 529 plans. Of the 35 states that offer tax deductions or credits on 529 plans, 22 currently have definitions that conform with the new federal definition. In some, statutory eligibility definitions were already linked to the federal definition, and so automatically conformed; others have passed legislation to conform.

The remaining legislation varies widely across states. Policymakers in some states with conforming definitions have introduced bills to limit eligible expenses to higher education; others have gone in the opposite direction, introducing bills to remove statutory language that currently put such limits in place. A few states are using this opportunity to create new college savings plans, or to add incentives and features to their 529 plans; others have introduced legislation to limit benefits if funds are used for K-12. Still others are requesting investigations into their state constitutions to see if the type of benefit expansion now allowed under the federal definition would be allowed in their state.

One thing is clear: In the middle of a busy legislative session, many state legislatures are looking to move policy on this issue. It will be interesting to see, once the dust settles, where states land on 529 plans.